4 minutes, 30 seconds read

Published on Jan 22, 2020

Updated on May 11, 2020

Create superior customer experiences to enhance competitive advantage.

Go from zero to breakthrough with scalable, future-proof solutions.

Harness deep tech for smarter solutions and maximum impact.

Accelerate value delivery with powerful pre-built digital tools.

Help businesses connect with an internet first generation.

Test the smarter way: where precision meets efficiency.

Unlock real-time and personalized customer journeys for mobile first generation.

Turn data into decisive action with scalable AI infrastructure.

Design agile digital foundations that scale with tomorrow's business needs.

Build new-age architecture for maximum efficiency and hyper-growth.

Fine-tune your cloud infrastructure for peak performance.

Automated compliance and control for global regulations.

All

Customer Experience

Mantra

Application Development

Insurtech

Digital Health

Insurance

Deep-Tech

AgriTech(1)

Augmented Reality(21)

Clean Tech(9)

Customer Journey(17)

Design(45)

Solar Industry(8)

User Experience(68)

Edtech(10)

Events(34)

HR Tech(3)

Interviews(10)

Life@mantra(11)

Logistics(6)

Manufacturing(5)

Strategy(18)

Testing(9)

Android(48)

Backend(32)

Dev Ops(11)

Enterprise Solution(33)

Technology Modernization(9)

Frontend(29)

iOS(43)

Javascript(15)

AI in Insurance(41)

Insurtech(67)

Product Innovation(59)

Solutions(22)

E-health(12)

HealthTech(25)

mHealth(5)

Telehealth Care(4)

Telemedicine(5)

Artificial Intelligence(154)

Bitcoin(8)

Blockchain(19)

Cognitive Computing(8)

Computer Vision(8)

Data Science(24)

FinTech(51)

Banking(7)

Intelligent Automation(27)

Machine Learning(48)

Natural Language Processing(14)

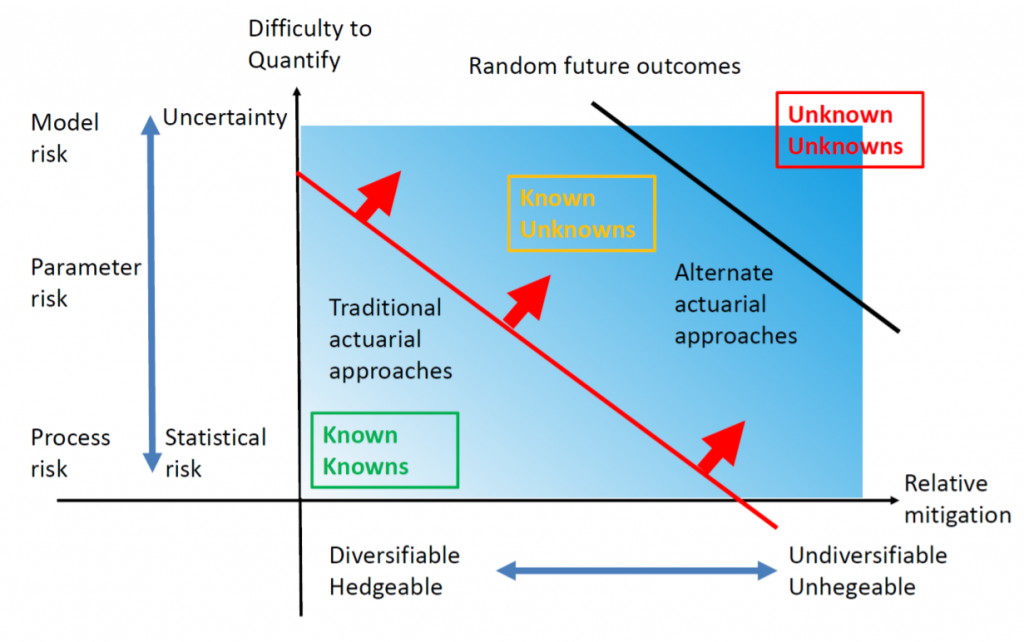

Ratemaking, or insurance pricing, is the process of fixing the rates or premiums that insurers charge for their policies. In insurance parlance, a unit of insurance represents a certain monetary value of coverage. Insurance companies usually base these on risk factors such as gender, age, etc. The Rate is simply the price per ‘unit of insurance’ for each unit exposed to liability.

Typically, a unit of insurance (both in life and non-life) is equal to $1,000 worth of liability coverage. By that token, for 200 units of insurance purchased the liability coverage is $200,000. This value is the insurance ‘premium’. (This example is only to demonstrate the logic behind units of exposure, and is not an exact method for calculating premium value)

The cost of providing insurance coverage is actually unknown, which is why insurance rates are based on the predictions of future risk.

Actuarial skills help measure the probability and risk of future events by understanding the past. They accomplish this by using probability theory, statistical analysis, and financial mathematics to predict future financial scenarios.

Insurers rely on them, among other reasons, to determine the ‘gross premium’ value to collect from the customer that includes the premium amount (described earlier), a charge for covering losses and expenses (a fixture of any business) and a small margin of profit (to stay competitive). But insurers are also subject to regulations that limit how much they can actually charge customers. Being highly skilled in maths and statistics the actuary’s role is to determine the lowest possible premium that satisfies both the business and regulatory objectives.

Source: Sam Gutterman, IAA Risk Book

Actuaries are essentially experts at managing risk, and owing to the fact that there are fewer actuaries in the World than most other professions — they are highly in demand. They lend their expertise to insurance, reinsurance, actuarial consultancies, investment, banking, regulatory bodies, rating agencies and government agencies. They are often attributed to the middle office, although it is not uncommon to find active roles in both the ‘front and middle’ office.

Recently, they have also found greater roles in fast growing Internet startups and Big-Tech companies that are entering the insurance space. Take Gus Fuldner for instance, head of insurance at Uber and a highly sought after risk expert, who has a four-member actuarial team that is helping the company address new risks that are shaping their digital agenda. In fact, Uber believes in using actuaries with data science and predictive modelling skills to identify solutions for location tracking, driver monitoring, safety features, price determination, selfie-test for drivers to discourage account sharing, etc., among others.

Also read – Are Predictive Journeys moving beyond the hype?

Within the General Actuarial practice of Insurance there are 3 main disciplines — Pricing, Reserving and Capital. Pricing is prospective in nature, and it requires using statistical modelling to predict certain outcomes such as how much claims the insurer will have to pay. Reserving is perhaps more retrospective in nature, and involves applying statistical techniques for identifying how much money should be set aside for certain liabilities like claims. Capital actuaries, on the other hand, assess the valuation, solvency and future capital requirements of the insurance business.

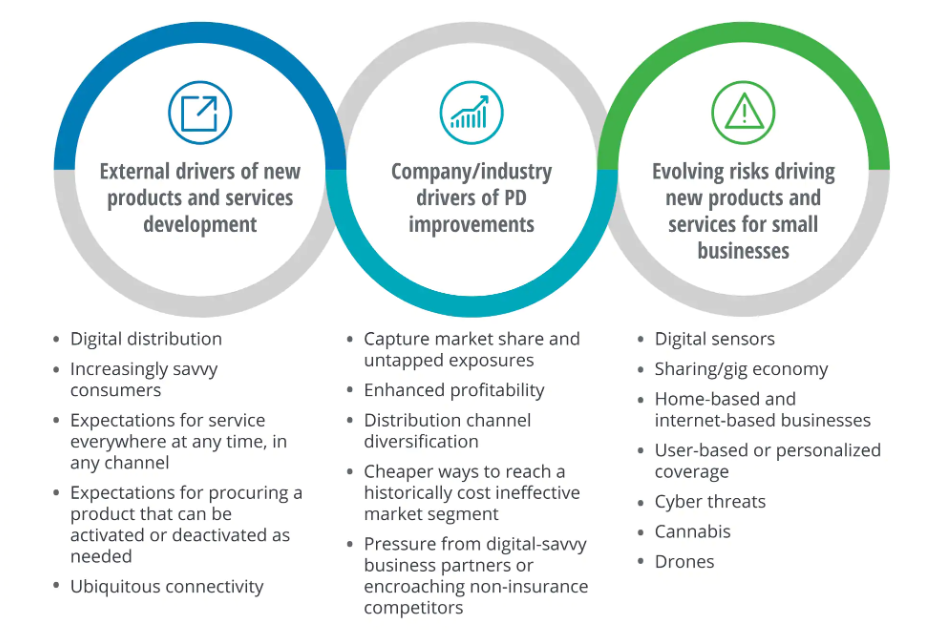

Insurance companies often respond to a growing market need or a potential technological disruptor when deciding new products/ tweaking old ones. They may be trying to address a certain business problem or planning new revenue streams for the organization. Typically, new products are built with the customer in mind. The more ‘benefit-rich’ it is, the easier it is to push on to the customer.

Normally, a group of business owners will first identify a broader business objective, let’s say — providing fire insurance protection for sub-urban, residential homeowners in North California. This may be a class of products that the insurer wants to open. In order to create this new product, they may want to study the market more carefully to understand what the risks involved are; if the product is beneficial to the target demographic, is profitable to the insurer, what is the expected value of claims, what insurance premium to collect, etc.

There are many forces external to the insurance company — economic trends, the agendas of independent agents, the activities of competitors, and the expectations and price sensitivity of the insurance market — which directly affect the premium volume and profitability of the product.

Source: Deloitte Insights

To determine insurance rate levels and equitable rating plans, ratemaking becomes essential. Statistical & forecasting models are created to analyze historical premiums, claims, demographic changes, property valuations, zonal structuring, and regulatory forces. Generalized linear models, clustering, classification, and regression trees are some examples of modeling techniques used to study high volumes of past data.

Based on these models, an actuary can predict loss ratios on a sample population that represents the insurer’s target audience. With this information, cash flows can be projected on the product. The insurance rate can also be calculated that will cover all future loss costs, contingency loads, and profits required to sustain an insurance product. Ultimately, the actuary will try to build a high level of confidence in the likelihood of a loss occurring.

This blog is a two-part series on new product development in insurance. In the next part, we will take a more focused view of the product development actuary’s role in creating new insurance products.

Knowledge thats worth delivered in your inbox

Smart Manufacturing starts with real-time visibility.

Manufacturing companies today generate data by the second through sensors, machines, ERP systems, and MES platforms. But without real-time insights, even the most advanced production lines are essentially flying blind.

Manufacturers are implementing real-time dashboards that serve as control towers for their daily operations, enabling them to shift from reactive to proactive decision-making. These tools are essential to the evolution of Smart Manufacturing, where connected systems, automation, and intelligent analytics come together to drive measurable impact.

Data is available, but what’s missing is timely action.

For many plant leaders and COOs, one challenge persists: operational data is dispersed throughout systems, delayed, or hidden in spreadsheets. And this delay turns into a liability.

Real-time dashboards help uncover critical answers:

By converting raw inputs into real-time manufacturing analytics, dashboards make operational intelligence accessible to operators, supervisors, and leadership alike, enabling teams to anticipate problems rather than react to them.

Line performance and downtime trends

Track OEE in real time and identify underperforming lines.

Predictive maintenance alerts

Utilize historical and sensor data to identify potential part failures in advance.

Inventory heat maps & reorder thresholds

Anticipate stockouts or overstocks based on dynamic reorder points.

Quality metrics linked to operator actions

Isolate shifts or procedures correlated with spikes in defects or rework.

These insights allow production teams to drive day-to-day operations in line with Smart Manufacturing principles.

Role-based dashboards

Dashboards can be configured for machine operators, shift supervisors, and plant managers, each with a tailored view of KPIs.

Embedded alerts and nudges

Real-time prompts, like “Line 4 below efficiency threshold for 15+ minutes,” reduce response times and minimize disruptions.

Cross-functional drill-downs

Teams can identify root causes more quickly because users can move from plant-wide overviews to detailed machine-level data in seconds.

Data lakehouse integration

Unified access to ERP, MES, IoT sensor, and QA systems—ensuring reliable and timely manufacturing analytics.

ETL pipelines

Real-time data ingestion from high-frequency sources with minimal latency.

Visualization tools

Custom builds using Power BI, or customized solutions designed for frontline usability and operational impact.

Mantra Labs partnered with a North American die-casting manufacturer to unify its operational data into a real-time dashboard. Fragmented data, manual reporting, delayed pricing decisions, and inconsistent data quality hindered operational efficiency and strategic decision-making.

As this case shows, real-time dashboards are not just operational tools—they’re strategic enablers.

(Learn More: Powering the Future of Metal Manufacturing with Data Engineering)

| Aspect | What You Should Know |

| 1. Why Static Reports Fall Short | Delayed insights after issues occur Disconnected systems (ERP, MES, sensors) No real-time alerts or embedded decision logic |

| 2. What Real-Time Dashboards Enable | Track OEE and downtime in real-time Predictive maintenance using sensor data Dynamic inventory heat maps Quality linked to operators |

| 3. Dashboards That Drive Action | Role-based views (operator to CEO) Embedded alerts like “Line 4 down for 15+ mins” Drilldowns from plant-level to machine-level |

| 4. What Powers These Dashboards | Unified Data Lakehouse (ERP + IoT + MES) Real-time ETL pipelines Power BI or custom dashboards built for frontline usability |

Smart Manufacturing dashboards aren’t just analytics tools—they’re productivity engines. Dashboards that deliver real-time insight empower frontline teams to make faster, better decisions—whether it’s adjusting production schedules, triggering preventive maintenance, or responding to inventory fluctuations.

Explore how Mantra Labs can help you unlock operations intelligence that’s actually usable.

Knowledge thats worth delivered in your inbox

Our Sales Team will be in touch with you shortly.

Hello Stranger! Please fill in a few details,and you’ll receive a link to this case study.

We have mailed you this case study.

We have mailed you this case study.

Thanks for subscribing.