Published on Jan 16, 2020

Updated on May 11, 2020

Create superior customer experiences to enhance competitive advantage.

Go from zero to breakthrough with scalable, future-proof solutions.

Harness deep tech for smarter solutions and maximum impact.

Accelerate value delivery with powerful pre-built digital tools.

Help businesses connect with an internet first generation.

Test the smarter way: where precision meets efficiency.

Unlock real-time and personalized customer journeys for mobile first generation.

Turn data into decisive action with scalable AI infrastructure.

Design agile digital foundations that scale with tomorrow's business needs.

Build new-age architecture for maximum efficiency and hyper-growth.

Fine-tune your cloud infrastructure for peak performance.

Automated compliance and control for global regulations.

All

Customer Experience

Mantra

Application Development

Insurtech

Digital Health

Insurance

Deep-Tech

AgriTech(1)

Augmented Reality(21)

Clean Tech(9)

Customer Journey(17)

Design(45)

Solar Industry(8)

User Experience(68)

Edtech(10)

Events(34)

HR Tech(3)

Interviews(10)

Life@mantra(11)

Logistics(6)

Manufacturing(5)

Strategy(18)

Testing(9)

Android(48)

Backend(32)

Dev Ops(11)

Enterprise Solution(33)

Technology Modernization(9)

Frontend(29)

iOS(43)

Javascript(15)

AI in Insurance(41)

Insurtech(67)

Product Innovation(59)

Solutions(22)

E-health(12)

HealthTech(25)

mHealth(5)

Telehealth Care(4)

Telemedicine(5)

Artificial Intelligence(154)

Bitcoin(8)

Blockchain(19)

Cognitive Computing(8)

Computer Vision(8)

Data Science(24)

FinTech(51)

Banking(7)

Intelligent Automation(27)

Machine Learning(48)

Natural Language Processing(14)

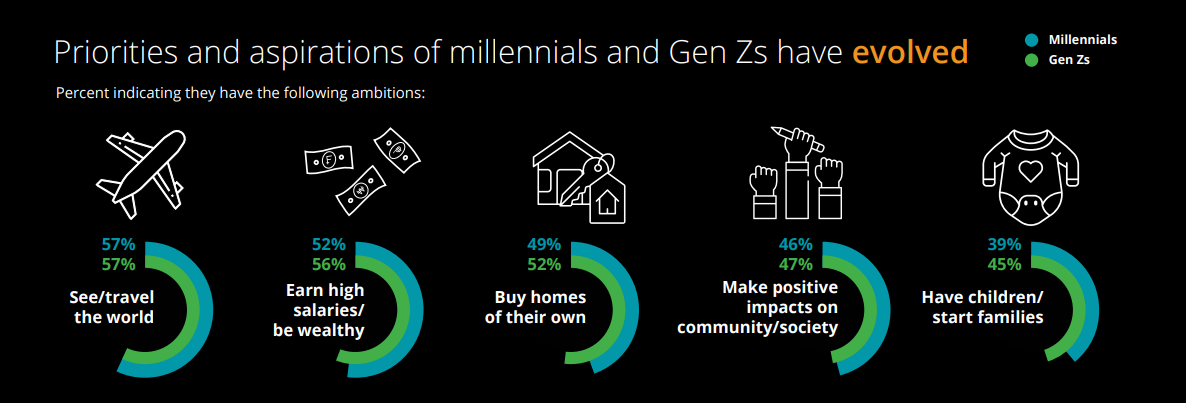

The insurance industry is changing and experts predict — nearly one-third of existing insurance models will disappear within this decade. The fierce competition, new opportunities with technologies like AI, and on top of that millennials’ changing preferences sum up to the call for more flexible and consumer-facing business models. Here are four new business models to set the insurance archetype.

Source: The Deloitte Global Millennial Survey 2019

Currently, AI is being used to strengthen the capabilities and knowledge of insurers and not consumers, creating information asymmetry. But, the question is — for how long will the consumers accept being a victim of ignorance.

A possible solution to this situation is bringing information transparency. It’s not like traditional insurers don’t share policy information with their customers. They do. However, lengthy policy documents and customers’ reliance on agents for information shadows the actual coverage, terms, etc. In a way, the information that customers receive becomes dependent on the agents’ knowledge and intentions.

Translating policy, terms and conditions documents into consumable bits of information with a clear distinction between what’s covered and what’s not will help in achieving transparency between insurers and customers.

For instance, Lemonade — the American Insurtech for renters and home insurance, disrupted the industry lately with their instant and transparent end-to-end insurance process. Their consumers are better aware of coverage and claims thanks to simplicity in the user experience.

Moreover, Lemonade donates the unclaimed premiums to social causes their consumers care about. From its inception in 2015 to date, Lemonade has sold over 1.2 million policies, in complete transparency and all through their AI bot — Maya!

Nearly 46% of millennials are willing to make a positive impact on the society/community. Lemonade has partnered with 92 charities and has donated $8,46,849 from unclaimed premiums. Hence, the answer.

Similarly, Swedish InsurTech Hedvig has successfully deployed it’s “nice insurance” services, giving back 80% of the unclaimed premiums to charities chosen by the customers.

More insights on — millennials and their expectations from insurance ‘beyond’ convenience.

Join our Webinar — AI for Data-driven Insurers: Challenges, Opportunities & the Way Forward hosted by our CEO, Parag Sharma as he addresses Insurance business leaders and decision-makers on April 14, 2020.

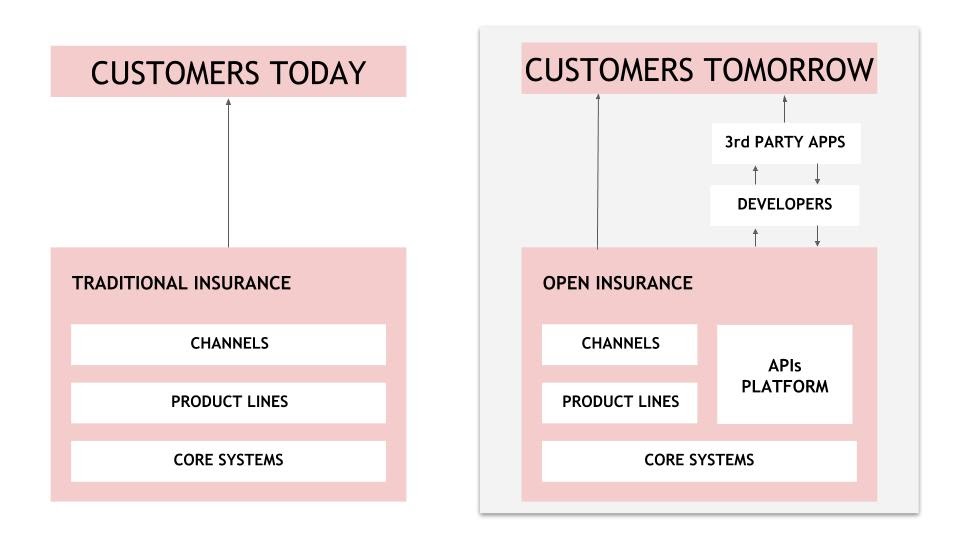

When user acquisition is the top priority, B2B2C or API-based model comes into action. Also known as an open-source platform solution, this business model connects people and processes with technology infrastructure and assets to manage user interactions.

In the API-based model, apart from traditional distribution channels, 3rd party apps also become a medium for customers to buy/access insurance policies. Automation plays a key role in this insurance model. Here, any other customer-centric digital application can install the API without manual/human intervention.

For example, in January 2018, Allianz announced that it will offer parts of its Allianz Business System (ABS) to other insurance companies for free. Interested organizations can simply install the API (Application Programming Interface, which is nothing but a chunk of software that connects two different apps) and start selling Allianz policies to their customers.

Lemonade — after disrupting the insurance space through transparency, has now stepped into this model. In October 2017, the company launched its public API, allowing anyone to distribute Lemonade’s policies through their websites or apps.

“It takes years to pull together the licenses, capital, and technology needed to offer insurance instantly through an app, which is why it’s almost nonexistent. Today’s API launch changes that. Anyone with a slight familiarity with coding can now include these capabilities in their app, in a matter of hours.”

Shai Wininger, Co-founder, President & COO, Lemonade

Unclaimed premiums also contribute to conflicts between insurers and policyholders. What if a customer is not interested in donating to charity, unlike mentioned in the above case?

Peer-to-Peer (P2P) insurance is perhaps an answer to eliminate premium settlement conflicts. It is also an emerging business model to access insurance coverage at lower costs than most of the traditional insurances.

This insurance model pools the individuals who share at least one relation — friends, family, or interest (community/clubs) and it serves two-fold benefits-

Also read – how behavioral psychology is fixing modern insurance claims

The notion of financial protection for the community has been prevalent in our societies since the 1600s. In the middle ages, the tradesmen followed the guild system (an association of craftsmen and merchants), where participants paid fees as a kind of insurance safety net. Though, the successful conceptualization of P2P insurance in the modern business models dates back to 2010 with German InsurTech — Friensurance. However, the P2P insurance model has credited the success to many more InsurTechs like Guevara, Axieme, TongJuBao (P2Pprotect), and PeerCover.

The greatest limiting factor for the success of microinsurance is distribution. For example, in the US, 18% of the premium represents the distribution cost, set aside marketing and advertising costs. Availability isn’t the issue for microinsurance.

The new business model for microinsurance focuses on outreaching and distributing policies at scale. Workflow automation solutions like document processing, automated customer query resolution, etc. make microinsurance models more effective.

The effectiveness of each of these models drills down to the smart use of technology in their implementations. Moreover, most of these business models are automated, thus, eliminating additional human resources for implementations. For instance, in India, an agent can charge up to 20% of the premium amount as fees, which can reduce significantly if the distribution is automated. Investment in technology for automating operations is also worth it because it makes customer outreach simpler and faster.

Also, read – 5 Front-office operations in Insurance you can automate with AI.

Knowledge thats worth delivered in your inbox

Smart Manufacturing starts with real-time visibility.

Manufacturing companies today generate data by the second through sensors, machines, ERP systems, and MES platforms. But without real-time insights, even the most advanced production lines are essentially flying blind.

Manufacturers are implementing real-time dashboards that serve as control towers for their daily operations, enabling them to shift from reactive to proactive decision-making. These tools are essential to the evolution of Smart Manufacturing, where connected systems, automation, and intelligent analytics come together to drive measurable impact.

Data is available, but what’s missing is timely action.

For many plant leaders and COOs, one challenge persists: operational data is dispersed throughout systems, delayed, or hidden in spreadsheets. And this delay turns into a liability.

Real-time dashboards help uncover critical answers:

By converting raw inputs into real-time manufacturing analytics, dashboards make operational intelligence accessible to operators, supervisors, and leadership alike, enabling teams to anticipate problems rather than react to them.

Line performance and downtime trends

Track OEE in real time and identify underperforming lines.

Predictive maintenance alerts

Utilize historical and sensor data to identify potential part failures in advance.

Inventory heat maps & reorder thresholds

Anticipate stockouts or overstocks based on dynamic reorder points.

Quality metrics linked to operator actions

Isolate shifts or procedures correlated with spikes in defects or rework.

These insights allow production teams to drive day-to-day operations in line with Smart Manufacturing principles.

Role-based dashboards

Dashboards can be configured for machine operators, shift supervisors, and plant managers, each with a tailored view of KPIs.

Embedded alerts and nudges

Real-time prompts, like “Line 4 below efficiency threshold for 15+ minutes,” reduce response times and minimize disruptions.

Cross-functional drill-downs

Teams can identify root causes more quickly because users can move from plant-wide overviews to detailed machine-level data in seconds.

Data lakehouse integration

Unified access to ERP, MES, IoT sensor, and QA systems—ensuring reliable and timely manufacturing analytics.

ETL pipelines

Real-time data ingestion from high-frequency sources with minimal latency.

Visualization tools

Custom builds using Power BI, or customized solutions designed for frontline usability and operational impact.

Mantra Labs partnered with a North American die-casting manufacturer to unify its operational data into a real-time dashboard. Fragmented data, manual reporting, delayed pricing decisions, and inconsistent data quality hindered operational efficiency and strategic decision-making.

As this case shows, real-time dashboards are not just operational tools—they’re strategic enablers.

(Learn More: Powering the Future of Metal Manufacturing with Data Engineering)

| Aspect | What You Should Know |

| 1. Why Static Reports Fall Short | Delayed insights after issues occur Disconnected systems (ERP, MES, sensors) No real-time alerts or embedded decision logic |

| 2. What Real-Time Dashboards Enable | Track OEE and downtime in real-time Predictive maintenance using sensor data Dynamic inventory heat maps Quality linked to operators |

| 3. Dashboards That Drive Action | Role-based views (operator to CEO) Embedded alerts like “Line 4 down for 15+ mins” Drilldowns from plant-level to machine-level |

| 4. What Powers These Dashboards | Unified Data Lakehouse (ERP + IoT + MES) Real-time ETL pipelines Power BI or custom dashboards built for frontline usability |

Smart Manufacturing dashboards aren’t just analytics tools—they’re productivity engines. Dashboards that deliver real-time insight empower frontline teams to make faster, better decisions—whether it’s adjusting production schedules, triggering preventive maintenance, or responding to inventory fluctuations.

Explore how Mantra Labs can help you unlock operations intelligence that’s actually usable.

Knowledge thats worth delivered in your inbox

Our Sales Team will be in touch with you shortly.

Hello Stranger! Please fill in a few details,and you’ll receive a link to this case study.

We have mailed you this case study.

We have mailed you this case study.

Thanks for subscribing.