3 minutes, 11 seconds read

Published on Oct 14, 2019

Updated on May 18, 2020

Create superior customer experiences to enhance competitive advantage.

Go from zero to breakthrough with scalable, future-proof solutions.

Harness deep tech for smarter solutions and maximum impact.

Accelerate value delivery with powerful pre-built digital tools.

Help businesses connect with an internet first generation.

Test the smarter way: where precision meets efficiency.

Unlock real-time and personalized customer journeys for mobile first generation.

Turn data into decisive action with scalable AI infrastructure.

Design agile digital foundations that scale with tomorrow's business needs.

Build new-age architecture for maximum efficiency and hyper-growth.

Fine-tune your cloud infrastructure for peak performance.

All

Customer Experience

Mantra

Application Development

Insurtech

Digital Health

Insurance

Deep-Tech

AgriTech(1)

Augmented Reality(21)

Clean Tech(9)

Customer Journey(17)

Design(45)

Solar Industry(8)

User Experience(68)

Edtech(10)

Events(34)

HR Tech(3)

Interviews(10)

Life@mantra(11)

Logistics(6)

Manufacturing(4)

Strategy(18)

Testing(9)

Android(48)

Backend(32)

Dev Ops(11)

Enterprise Solution(33)

Technology Modernization(9)

Frontend(29)

iOS(43)

Javascript(15)

AI in Insurance(41)

Insurtech(67)

Product Innovation(59)

Solutions(22)

E-health(12)

HealthTech(25)

mHealth(5)

Telehealth Care(4)

Telemedicine(5)

Artificial Intelligence(154)

Bitcoin(8)

Blockchain(19)

Cognitive Computing(8)

Computer Vision(8)

Data Science(23)

FinTech(51)

Banking(7)

Intelligent Automation(27)

Machine Learning(48)

Natural Language Processing(14)

People concerned with insurance have been using the terms- ‘innovation’ and ‘disruption’ interchangeably, perhaps because both correspond to building something ‘new’. However, there is a fine line between the two. All disruptors are innovators whereas, not all innovators are disruptors. Let’s delve deep into the difference between disruption and innovation in insurance.

Disruptors drastically alter prevalent businesses, services, or products. They tend to be more creative, useful, impactful, inexpensive, time-savvy, and most importantly – scalable.

As an example, Lemonade took in $57 million in premium revenue from 4,25,000 customers in 2018. This four-year-old startup was able to sell premiums to millennials- 90% of whom were purchasing insurance for the first time.

Reason- instead of an all-encompassing insurance package, Lemonade is keen on distributing micro policies as low as $5, which the customer perceives as useful. They’ve simplified the claim settlement process and within 3 minutes, a customer can get his refund credited to his account. While Lemonade sells its insurance policies through chatbot Maya, chatbot Jim handles claim settlement. Such AI-powered bots can handle multiple customer requests just as human agents and are better in detecting fraud.

The disruptors are prone to adapt to changing customer preferences, which the traditional insurers are reluctant to because of the fear of losing existing customers. Disruption in insurance can break the barrier of the lower market penetration rate.

Innovation is independent of drastic changes in businesses. It focuses more on bringing positive business development by delivering convenience to the customer and improving operational efficiency.

Innovation is not always about introducing new technology. It is also about harnessing existing technologies to build innovative solutions. For instance, blockchain technology has been there for decades; but the insurance industry has recently utilized it for algorithmic trading, smart contracts, policy distribution, and claim settlements.

For example, AXA Fizzy provides paperless flight insurance based on blockchain technology. Every user interaction is recorded and executed in the ledgers- from buying a policy to claim settlement without any human intervention.

Other examples of innovation in insurance include Robo-advice, NLP (Natural Language Processing) to understand customer queries, insurance for IoT devices, AI-powered underwriting, automating insurance workflows, and Machine Learning technologies.

Also, read – Innovative insurance products of 2109.

However, according to McKinsey’s report on Digital insurance in 2018, most of the P&C, health, and life insurance innovations revolve around marketing and less towards product development and claims. This gives an idea of the scope of innovation in insurance.

The traditional insurance business is known to be resilient to technological advancements and innovations in terms of consumer-centric products. To stay relevant and competitive, insurers should shift focus from digitization to strategic disruption according to the changing market dynamics.

In fact, Insurers are willing to fund insurance startups to gain a first-mover advantage in terms of technology and innovations. These investments illustrate a clear goal of improving customer experiences and supporting their existing operations at the startups’ risk.

For instance, “Axa provided seed funding for five European start-ups under a fund set up in France in 2013, before launching Axa Strategic Ventures in 2015. The €200 million ($223.47 million) venture capital fund has the mandate to invest in innovations in insurance..”. (OECD (2017), Technology and innovation in the insurance sector)

Innovation from Insurtechs has the potential to contribute to the insurance value chain; however, managing disruption is still quite a challenge. Disruption alters the business and behaviours in such a short span that most of the outcomes remain unanticipated. While innovation takes time to catch the stream, disruption can make or kill a business. The best is to blend incumbents’ years of experience with innovation from startups to bring an accountable disruption.

We’ve been solving critical front & back-office insurtech challenges through innovative technological solutions. Drop us a ‘hi’ at hello@mantralabsglobal.com to know more.

Knowledge thats worth delivered in your inbox

Claims are the moment of truth. Are you turning them into moments of loyalty?

In insurance, your app interface might win you downloads. Your pricing might drive conversions.

But it’s the claims experience that decides whether a customer stays—or leaves for good.

According to a survey by NPS Prism, promoters are 2.3 times more likely to renew their insurance policies than passives or detractors—highlighting the strong link between customer advocacy and retention.

NPS in insurance industry is a strong predictor of customer retention. Many insurers are now prioritizing NPS to improve their claims experience.

So, what are today’s high-NPS insurers doing differently? Spoiler: it’s not just about faster payouts.

We’ve worked with claims teams that had best-in-class automation—but still had low NPS. Why? Because the process felt like a black box.

Customers didn’t know where their claim stood. They weren’t sure what to do next. And when money was at stake, silence created anxiety and dissatisfaction.

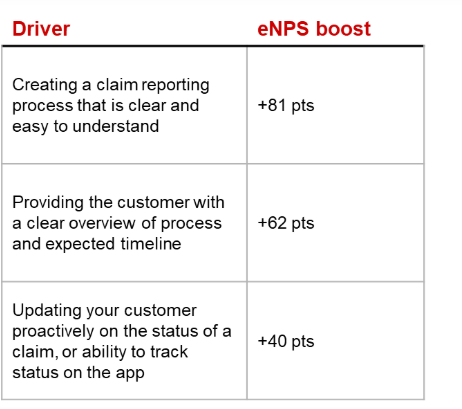

Great customer experience (CX) in claims isn’t just about speed—it’s about giving customers a sense of control through clear communication and clarity.

The result? Frustrated customers and overwhelmed call centers.

Customers don’t always expect instant decisions. What they want:

Transparency to the customer via mobile app, email, or WhatsApp—keeping them in the loop with clear milestones.

Auto-reminders, such as “upload your medical bill” or “submit police report,” help close matters much faster and avoid back-and-forth.

Single-click scans with OCR + AI pull data instantly—no typing, no errors.

Simple post-resolution surveys collect sentiment and alert on issues in real time.

For e.g., Lemonade uses emotional AI to detect customer sentiment during the claims process, enabling empathetic responses that boost satisfaction and trust.

For a leading insurance firm, we mapped the entire in-app user journey—from buying or renewing a policy to initiating a claim or checking discounts. This helped identify exactly where users dropped off. Based on real-time activity, we triggered personalized notifications and offers—driving better engagement and claim completion rates.

What do insurers gain from investing in CX?

A faster claim is good. But a fair, clear, and human one wins loyalty.

And companies that consistently track and act on CX metrics are better positioned to retain customers and build long-term loyalty.

At Mantra Labs, we help insurers build end-to-end, tech-enabled claims journeys that delight customers and drive operational efficiency.

From intelligent document processing to AI-led nudges, we design for empathy at scale.

Let’s design it together.

Talk to our insurance transformation team today.

Knowledge thats worth delivered in your inbox

Our Sales Team will be in touch with you shortly.

Hello Stranger! Please fill in a few details,and you’ll receive a link to this case study.

We have mailed you this case study.

We have mailed you this case study.

Thanks for subscribing.