Published on Aug 6, 2019

Updated on Dec 13, 2019

Create superior customer experiences to enhance competitive advantage.

Go from zero to breakthrough with scalable, future-proof solutions.

Harness deep tech for smarter solutions and maximum impact.

Accelerate value delivery with powerful pre-built digital tools.

Help businesses connect with an internet first generation.

Test the smarter way: where precision meets efficiency.

Unlock real-time and personalized customer journeys for mobile first generation.

Turn data into decisive action with scalable AI infrastructure.

Design agile digital foundations that scale with tomorrow's business needs.

Build new-age architecture for maximum efficiency and hyper-growth.

Fine-tune your cloud infrastructure for peak performance.

All

Customer Experience

Mantra

Application Development

Insurtech

Digital Health

Insurance

Deep-Tech

AgriTech(1)

Augmented Reality(21)

Clean Tech(9)

Customer Journey(17)

Design(45)

Solar Industry(8)

User Experience(68)

Edtech(10)

Events(34)

HR Tech(3)

Interviews(10)

Life@mantra(11)

Logistics(5)

Manufacturing(3)

Strategy(18)

Testing(9)

Android(48)

Backend(32)

Dev Ops(11)

Enterprise Solution(33)

Technology Modernization(9)

Frontend(29)

iOS(43)

Javascript(15)

AI in Insurance(38)

Insurtech(66)

Product Innovation(58)

Solutions(22)

E-health(12)

HealthTech(24)

mHealth(5)

Telehealth Care(4)

Telemedicine(5)

Artificial Intelligence(153)

Bitcoin(8)

Blockchain(19)

Cognitive Computing(8)

Computer Vision(8)

Data Science(23)

FinTech(51)

Banking(7)

Intelligent Automation(27)

Machine Learning(48)

Natural Language Processing(14)

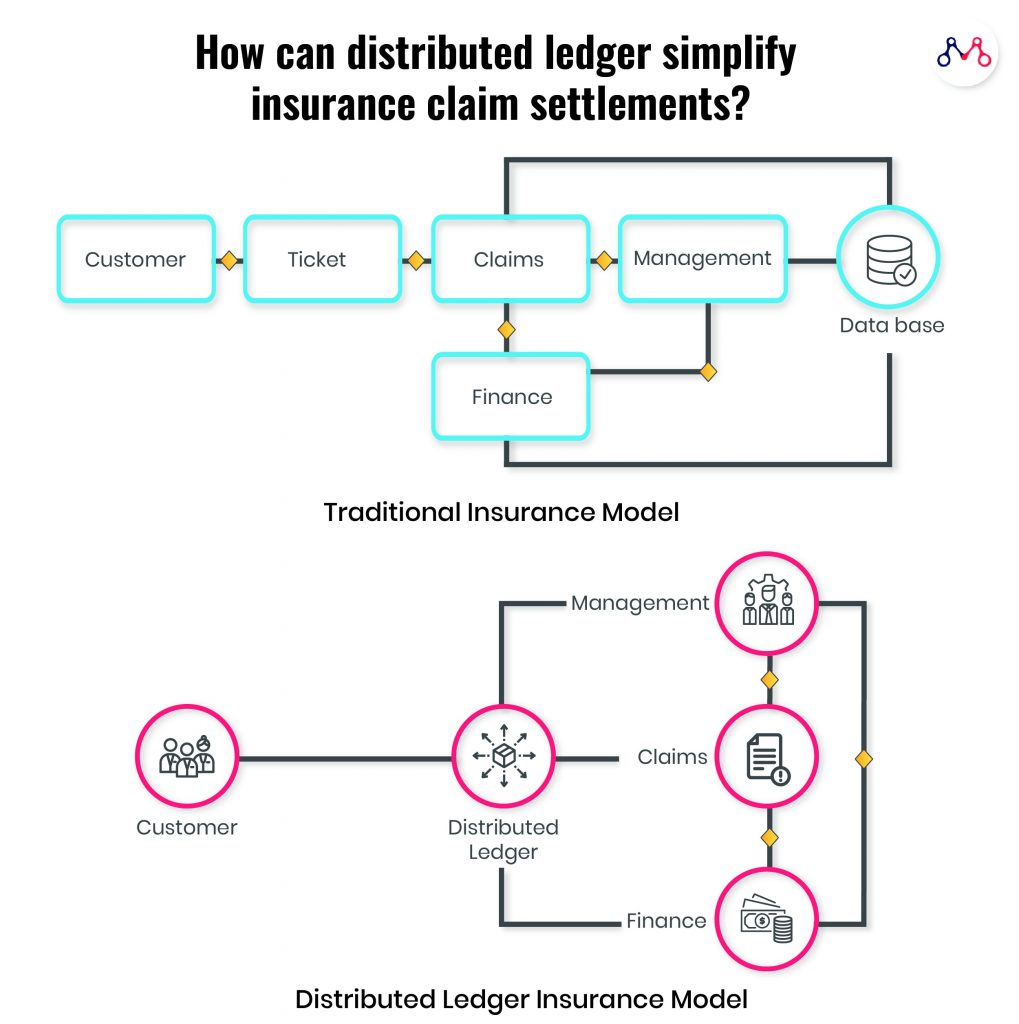

The years 2018-19 are the banner years for the US$ 5.17 trillion global insurance sector. However double-booking, counterfeiting, and premium diversions through unlicensed brokers still throb insurance companies. And one of the prime reasons for such unethical activities is the lack of tight coupling between stakeholders. A simple solution to these challenges is distributed ledgers- a contemporary technology that ensures transparency. Distributed ledger technology in insurance can create a collaborative environment for handling information, minimizing instances of fraudulent activities.

Where most insurtech startups and small insurers are looking for “insurance-in-a-box” technology, big players demand bespoke technology to develop distinct capabilities for customer convenience and manage their enterprise workflows. Fortunately, distributed ledger technology solves a major chunk of this problem.

For startups and small to medium size insurtech firms, cloud-based, customizable workflow management products can simplify the processes and create a collaborative work environment. Large enterprises can, of course, afford time and investment for tailor-made technologies suitable for their overall business requirements.

Smart contracts can automatically determine whether to transfer an asset to the nominee or back to the source, or a combination of both. It does not necessarily create a contract or legal act, but can sure validate a condition. For example, Ethereum provides a prominent smart contract framework.

Smart contracts allow credible transactions with or without involving third parties (oracles).

For example, Etherisc uses smart contracts concepts for building insurance products. The fundamentals used for Etherisc’s insuring flight delays product is applicable for insurance products like crop insurance, flood, earthquake, etc.

Cifas reports a 27% rise in false insurance claims across the UK in the past year. Moreover, insurers identify 1 in every 30 claims as fraudulent. Organizations can track records better with distributed ledgers minimizing the illicit instances.

Blockchain technology allows for automated real-time data collection and analysis. BCG expects Property and Casualty (P&C) insurance has the potential of processing claims up to 3x faster and 5x cheaper than traditional processes.

It can also enhance customer experience by removing indirections due to various touchpoints between him and the claim settlement manager. Distributed ledgers can overall benefit processing time, automating payments, eliminating trust issues, and fraud reduction.

Reinsurance (passing a whole or part of insurance liabilities to another company) will simplify the sharing of data like bordereau and claims databases. For the insurance companies not preferring to share their client’s data, access rights can be customized in distributed ledgers.

According to PWC research, the reinsurance industry can save up to $10B by increasing operational efficiencies through distributed ledgers.

“A shared, distributed ledger lends itself to this need for exchanging transparent, trustworthy data in a standard format in real-time.”

Stefan Schrijnen: Director, Insurance, EY

Having accurate real-world data can help underwriters reduce paperwork and measure the assets and risks effectively.

Insurwave, a blockchain-enabled insurance platform uses a distributed database with secure access for insuring shipments across the world. Maersk, the world’s leading shipping and logistics company have partnered with Insurwave for insurance renewal of its fleet of 800 container ships.

In the words of Lars Henneberg, Head of Risk Management at A.P. Moller – Maersk. “A simple dashboard gives us a live overview of how our assets are insured, and our brokers and insurers have access to the same overview. If the location, cargo, or other data about our ships changes, everyone is notified — no delays, no paperwork, no mistakes.”

Instead of all-encompassing insurance policies, consumers look for short, custom-built policies that satisfy their immediate needs. Therefore, to stay competitive, insurance companies (and even e-commerce startups) need to consistently build new and relevant insurance products. Expanding features or building new products on the same fundamentals can be effectively realized with strong and transparent ledgers.

AXA’s smart contract product Fizzy is a next-generation Parametric Insurer, which uses transparency as its USP. It provides travel insurance on flight delays and cancellations. The claims displayed on the website are stored in a blockchain and no one can change the terms after purchase. User can buy the insurance online. When the flight is delayed or canceled, the public databases of plane status information automatically triggers the insurance holder’s compensation. The event confirmation executes and closes the claim process instantly.

MarketsandMarkets expects blockchain technology’s share in the insurance market to reach $1.4 billion by 2023.

The insurance industry has already deployed distributed ledger components for insuring flight delays, lost baggage claims, and is expanding to shipping, health, and consumer durables domains.

The future can also witness blockchain, AI, drones, and robotics disrupting the insurance industry together.

Knowledge thats worth delivered in your inbox

AI code assistants are revolutionizing software development, with Gartner predicting that 75% of enterprise software engineers will use these tools by 2028, up from less than 10% in early 2023. This rapid adoption reflects the potential of AI to enhance coding efficiency and productivity, but also raises important questions about the maturity, benefits, and challenges of these emerging technologies.

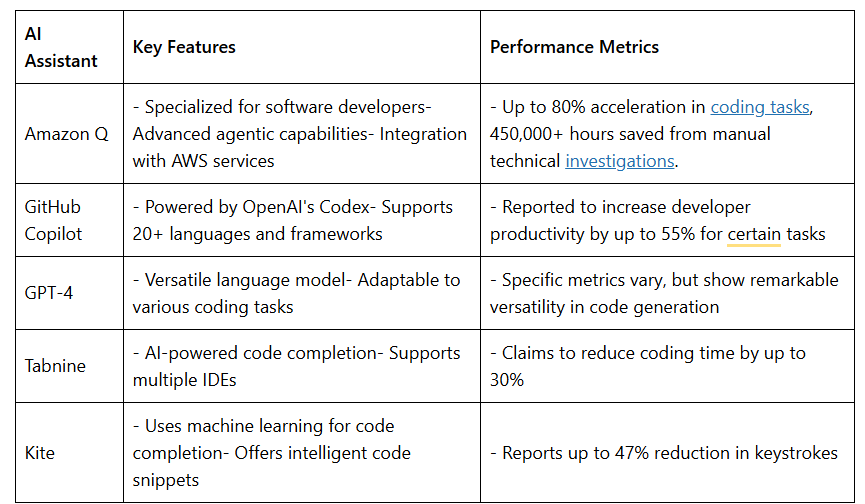

The evolution of code assistance has been rapid and transformative, progressing from simple autocomplete features to sophisticated AI-powered tools. GitHub Copilot, launched in 2021, marked a significant milestone by leveraging OpenAI’s Codex to generate entire code snippets 1. Amazon Q, introduced in 2023, further advanced the field with its deep integration into AWS services and impressive code acceptance rates of up to 50%. GPT (Generative Pre-trained Transformer) models have been instrumental in this evolution, with GPT-3 and its successors enabling more context-aware and nuanced code suggestions.

These advancements have not only increased coding efficiency but also democratized software development, making it more accessible to novice programmers and non-professionals alike.

The landscape of AI code assistants is rapidly evolving, with adoption rates and performance metrics showcasing their growing maturity. Here’s a tabular comparison of some popular AI coding tools, including Amazon Q:

Amazon Q stands out with its specialized capabilities for software developers and deep integration with AWS services. It offers a range of features designed to streamline development processes:

The tool’s impact is evident in its adoption and performance metrics. For instance, Amazon Q has helped save over 450,000 hours from manual technical investigations. Its integration with CloudWatch provides valuable insights into developer usage patterns and areas for improvement.

As these AI assistants continue to mature, they are increasingly becoming integral to modern software development workflows. However, it’s important to note that while these tools offer significant benefits, they should be used judiciously, with developers maintaining a critical eye on the generated code and understanding its implications for overall project architecture and security.

AI code assistants are revolutionizing collaborative coding practices, offering real-time suggestions, conflict resolution, and personalized assistance to development teams. These tools integrate seamlessly with popular IDEs and version control systems, facilitating smoother teamwork and code quality improvements.

Key features of AI-enhanced collaborative coding:

Benefits for development teams:

While AI code assistants offer significant advantages, it’s crucial to maintain a balance between AI assistance and human expertise. Teams should establish guidelines for AI tool usage to ensure code quality, security, and maintainability.

Emerging trends in AI-powered collaborative coding:

As AI continues to evolve, collaborative coding tools are expected to become more sophisticated, further streamlining team workflows and fostering innovation in software development practices.

AI code assistants offer significant benefits but also present notable challenges. Here’s an overview of the advantages driving adoption and the critical downsides:

Core Advantages Driving Adoption:

| Industry | Potential Annual Value |

| Banking | $200 billion – $340 billion |

| Retail and CPG | $400 billion – $660 billion |

Critical Downsides and Risks:

While AI code assistants offer significant productivity gains and economic benefits, they also present challenges that need careful consideration. Developers and organizations must balance the advantages with the potential risks, ensuring responsible use of these powerful tools.

The future of AI code assistants is poised for significant growth and evolution, with technological advancements and changing developer attitudes shaping their trajectory towards potential ubiquity or obsolescence.

Technological Advancements on the Horizon:

Barriers:

Enablers:

As these trends unfold, the role of human developers is likely to shift towards higher-level problem-solving, creative design, and AI oversight. By 2025, it’s projected that over 70% of professional software developers will regularly collaborate with AI agents in their coding workflows1. However, the path to ubiquity will depend on addressing key challenges such as reliability, security, and maintaining a balance between AI assistance and human expertise.

The future outlook for AI code assistants is one of transformative potential, with the technology poised to become an integral part of the software development landscape. As these tools continue to evolve, they will likely reshape team structures, development methodologies, and the very nature of coding itself.

AI code assistants have irrevocably altered software development, delivering measurable productivity gains but introducing new technical and societal challenges. Current metrics suggest they are transitioning from novel aids to essential utilities—63% of enterprises now mandate their use. However, their ascendancy as the de facto standard hinges on addressing security flaws, mitigating cognitive erosion, and fostering equitable upskilling. For organizations, the optimal path lies in balanced integration: harnessing AI’s speed while preserving human ingenuity. As generative models evolve, developers who master this symbiosis will define the next epoch of software engineering.

Knowledge thats worth delivered in your inbox

Our Sales Team will be in touch with you shortly.

Hello Stranger! Please fill in a few details,and you’ll receive a link to this case study.

We have mailed you this case study.

We have mailed you this case study.

Thanks for subscribing.